With all the talk of rising home prices, buyers who’ve been dreaming of getting into a new home are starting to question if it is still affordable to buy.

There’s no denying the increase in property values over the past year – but it’s not the only determinant to home affordability.

Keep reading to learn what factors contribute to housing affordability!

Affordability Factors

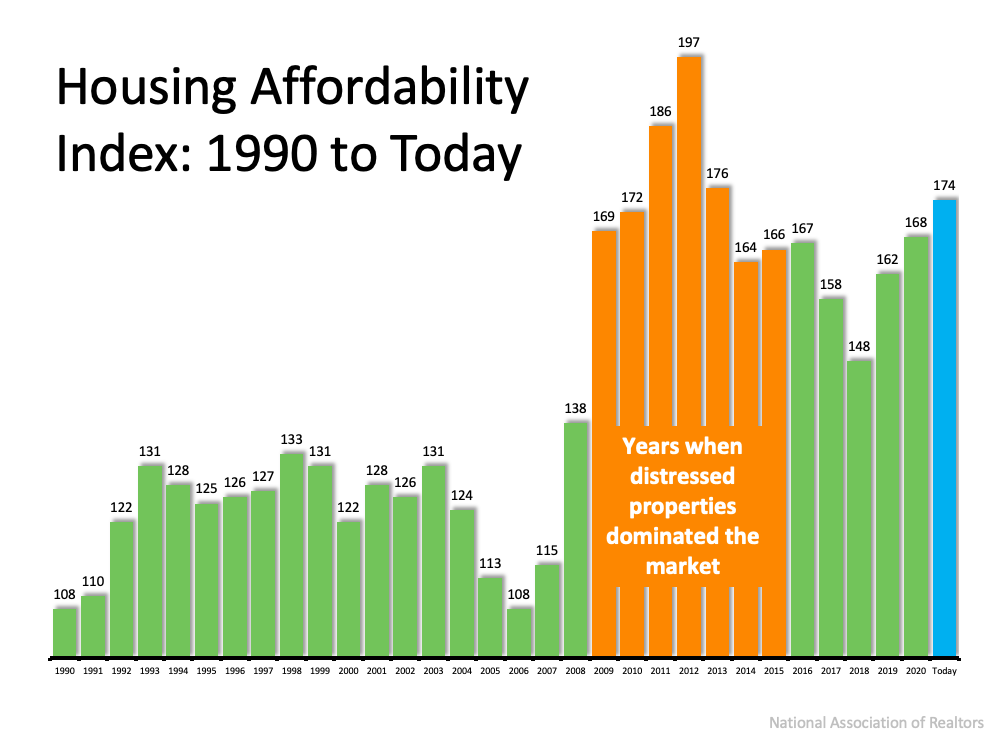

NAR’s Housing Affordability takes three factors into account when determining a housing affordability score:

- Mortgage Rates

- Mortgage Payments as a Percentage of Income

- Home Prices

The higher the score – the more affordable it is to purchase a home. We can see that homes are more affordable now than at any point other than 2011-2013, when distressed properties dominated the market following the housing crash.

The largest factor in today’s homebuying affordability is historically low mortgage rates.

Because of this, it’s actually MORE affordable to buy a home today than at any time in the last 8 years!

Your Personal Financial Situation

In addition to the three main factors that NAR looks at when determining affordability, you also need to consider your personal financial situation.

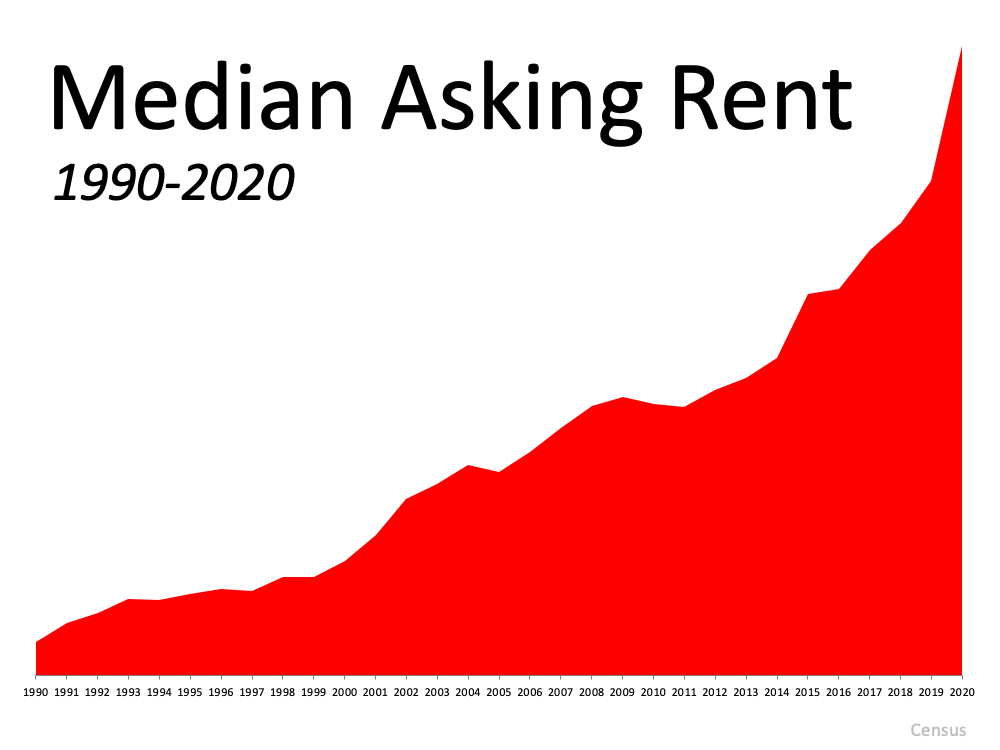

People who rent generally spend a higher percentage of their income toward a rental payment than homeowners do toward a mortgage, according to Homeownership is Affordable Housing, a report by Urban Institute. Because renters spend a higher percentage of their income, they don’t have extra money to invest in other assets.

In addition, your mortgage payment will remain relatively the same over time, while rent prices continue to increase. This means renters will continually spend a higher percentage of their income, even as they begin to make more money.

Wondering if buying a home is within your reach this year? Contact us today!